I believe that CVS Health (NYSE:CVS) is downright undervalued and is trading at a discount of 57%. The completion of the Aetna (NYSE:AET) acquisition would solidify revenue growth and allow CVS to diversify its streams of revenue. Such an acquisition could certainly provide the groundwork for larger revenue growth as well as an increase in long-term debt.

How is CVS growing?CVS is the largest retail pharmacy in the United States, currently boasting nearly 20,000 pharmacies. As the US population ages and grows, the demand for pharmaceutical prescriptions is rising. Based on listing prices, spending on pharmaceuticals in 2016 totaled approximately $450 billion. This spending on prescriptions is expected to accelerate and total approximately $600 billion by 2021, which would allow CVS to capitalize, considering approximately 45% of its revenue is generated through filling prescription medications.

The AET acquisition would mean the absorption of the 3rd largest health insurer in the United States. This would allow for cheaper prescriptions as CVS's pharmacy benefit management, which allows CVS to negotiate prices with different insurers, would lower prices for those insured by the health insurance wing of the pharmaceutical retain giant. There are currently 22 million Americans insured by AET who would then have the price incentive to fill their prescriptions at CVS. Currently, AET brings in approximately 60$ billion annually, and that is projected to rise at an average of 5% through 2022. This extra income can help CVS diversify its revenue streams and pull ahead of its competition as it faces threats in Walmart (NYSE:WMT) and Amazon (NASDAQ:AMZN).

Debt ProblemsCurrent long-term debt for CVS sits at $65.1 billion, which was ballooned through CVS's attempt to acquire AET. CVS's credit rating sits at Baa1. However, Moody's Investor Services have held CVS's credit rating on review, and the result could very well end in a Baa2 rating, approaching junk bond territory. The operating cash flow for CVS covers approximately 10% of current long-term debt, which sits below the normal healthy amount of debt, 20%. Despite this, I believe that CVS is still financially stable. However, the cost will dampen cash flow and hurt CVS. EBIT coverage on necessary interest payments is approximately 8.4x. CVS has the ability to pay down its long-term debt and, as a result, raise its cash flow.

CompetitionCVS will still continue to face competition from Walgreens (WBA) and Rite Aid (NYSE:RAD). However, it is other companies that may pose a bigger challenge in the near future. WMT is currently in early-stage acquisition talks with Humana (NYSE:HUM), which would allow WMT to effectively compete with CVS, assuming their respective mergers are approved. WMT has recently received a patent on blockchain technology-based data systems for medical records. This is significant because this technology that WMT has patented could allow first responders to access medical information of people who are unable to communicate. HUM is currently the fourth largest health insurance company in the United States, bringing in $54.3 billion in net revenue. AMZN has begun to enter the healthcare market through a partnership with Berkshire Hathaway (NYSE:BRK.A) and JPMorgan (NYSE:JPM). This new venture aims to reduce the cost of healthcare services by cutting out middlemen and other sources of waste. Dr. Atul Gawande was named the CEO of their newly formed healthcare company. A large part of their strategy seems to be going after pharmacy benefit management, which would mean that CVS would have to lower prices in order to compete, at the very least.

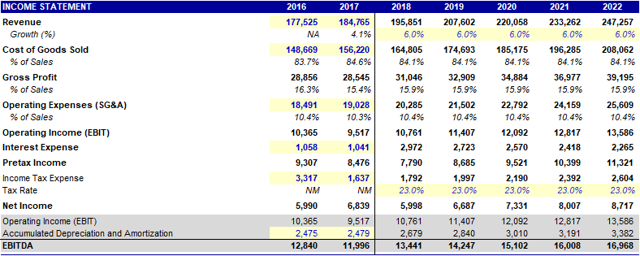

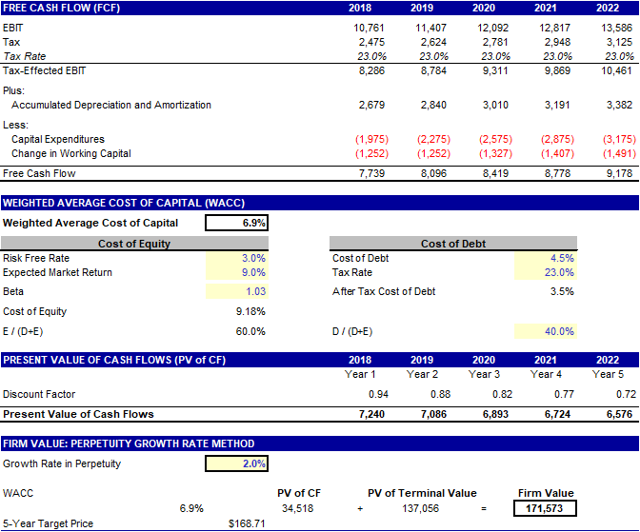

ValuationAccording to my discounted cash flow analysis, CVS is trading at a discount of 57%. I've projected sales growth at an average of 6% over the next 5 years, which accounts for growing threats in the PBM and retail industry. This growth will heavily be a result of the growth in prescriptions and the need for them to be filled.

This leads me into my discounted cash flow model, in which I use the perpetuity growth method. I've calculated by beta through monthly comparison with CVS and the S&P 500 since 2012 and assumed a growth rate in perpetuity at 2%.

At a WACC of 6.9%, CVS is extremely undervalued and is trading well below what it should be considering its future outlook. Free cash flow will steadily rise and prove to raise the company's valuation.

CVS's P/E ratio is 10.8x, which is well below the healthcare industry average of 21.9x and the current market average of 18.4x. This is yet another example of how CVS is trading at a discount.

Note that this valuation does not take into account the prospective AET merger, which would fundamentally change CVS and assuredly provide a more weighted valuation.

Dividend YieldCurrent dividend yield sits at 2.83%, resulting in $2 per share. Current analyst projections point to a dividend yield growth to 3.55% by 2021, which could yield $2.51 per share. This dividend yield is not particularly high in comparison with the market as a whole. However, someone looking to diversify their income investing portfolio could look to the pharmaceutical retail industry, and CVS stands out in that regard as they boast a higher dividend yield than its closest competitors WBA and RAD (as RAD does not pay dividends).

ConclusionI believe that CVS is extremely undervalued at its current price, and there is a large amount of upside that CVS will see if regulators approve the AET deal. The dividend yield that CVS offers is simply a cherry on top to the rest of CVS's strengths. While there are some growing pains that CVS suffers from their on-boarding of debt, I believe CVS can handle its debt levels well and provide strong growth over the next 5 years, allowing CVS to reach its fair value.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in CVS over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Note: I am a sophomore at The University of Alabama. Please leave any criticisms, corrections, or notes to help me better my overall investing acumen in the comment section below. Thank you for reading my article!

No comments:

Post a Comment